![]()

Neurodiagnostics Market to Surge from USD 10.52B in 2026 to USD 20.36B by 2035- Powered by Government Neurotech Funding, AI-Augmented Diagnostic Workflows

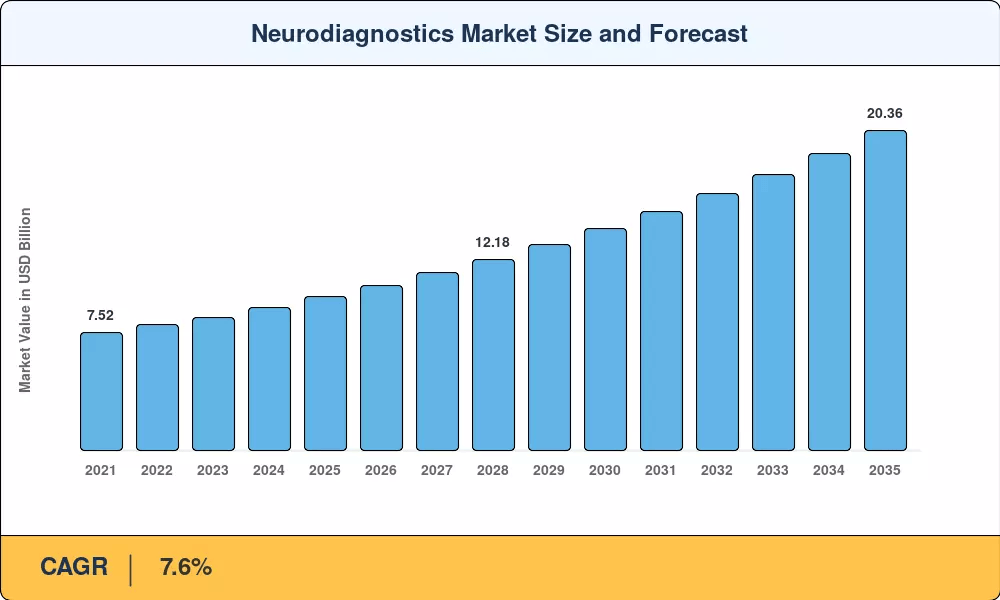

NY, CA, UNITED STATES, June 24, 2026 /EINPresswire.com/ — As per Market Research Future, the global Neurodiagnostics Market size is projected to reach USD 20.36 Billion by 2035 from USD 10.52 Billion in 2026, at a CAGR of 7.6% during the forecast period 2026–2035. The market base was estimated at USD 9.78 Billion in 2025.

The 7.6% CAGR—anchored by structural neurological disease burden rather than discretionary healthcare spending—is driven by three converging forces: large-scale government neurotech funding programs that continue to widen the addressable base for advanced diagnostics, sustained AI-augmented diagnostic workflow adoption that has pulled legacy film-based imaging suites and stand-alone electroencephalography consoles into cloud-enabled, real-time analytics platforms, and the technological shift from invasive, high-cost PET imaging toward blood-based biomarker panels for amyloid and tau proteins that provide clinicians with faster, less intrusive means of detecting neurodegenerative diseases at early stages.

National governments and multilateral health organizations are amplifying this momentum. The U.S. National Institutes of Health committed over USD 12 billion to the BRAIN Initiative through 2026, while the European Commission’s Horizon Europe program earmarked EUR 1.8 billion for neuroscience and digital-health research through 2027.

Request A Free Sample:

https://www.marketresearchfuture.com/sample_request/8762

Key Market Trends & Growth Drivers

Aging Population and Neurodegenerative Disease Burden

The WHO projects that the global population aged 65 and older will double from 761 million in 2021 to 1.6 billion by 2050. Alzheimer’s disease alone affects an estimated 55 million people worldwide, with annual diagnostic and care costs exceeding USD 1.3 trillion.

This demographic pressure generates sustained, non-cyclical demand for the Neurodiagnostics Market, as healthcare systems shift toward early detection to reduce long-term treatment costs. Countries with the most pronounced aging curves—Japan, Germany, Italy, and South Korea—are allocating targeted public funds to expand diagnostic access in primary-care settings. Each percentage point of aging-population growth translates into measurable diagnostic volume, and the neurodegenerative disease screening embedded in routine geriatric care makes this driver structurally durable through 2035.

AI-Augmented Diagnostic Workflows and Cloud-Enabled Platforms

The FDA cleared 171 AI-enabled medical devices in 2023, with neurology and radiology representing significant segments of this growth. AI-driven interpretation tools are increasingly adopted to streamline workflows, assisting in the triage of neuroimaging and the identification of neurological anomalies.

By augmenting the capacity of clinical teams, these tools help address the global challenge of specialist shortages and the rising volume of neuroimaging studies, positioning AI as a crucial operational multiplier for the Neurodiagnostics Market.

Blood-Based Biomarker Commercialization and Precision Neurology

Blood-based biomarkers, particularly those measuring phosphorylated-tau (p-tau217), are rapidly transitioning from research settings into clinical practice. Following the FDA clearance of several commercial p-tau217 assays in 2025, these tests have emerged as a scalable alternative to PET imaging for assessing amyloid pathology.

While PET scans remain a gold standard with costs often exceeding USD 5,000, blood-based panels offer a significantly more accessible and cost-effective screening modality ranging from USD 200–400 per test. The market is currently undergoing a shift as clinical guidelines integrate these tests into routine diagnostic workups throughout 2026–2028.

Ask for Customization:

https://www.marketresearchfuture.com/ask_for_customize/8762

Market Segment Insights

BY PRODUCT TYPE

Reagents & Consumables: Dominant segment with ~54.6% revenue share in 2025. Reflecting recurring procurement cycles across hospital and reference laboratories for biomarker assay kits, electrode supplies, and contrast agents on predictable schedules tied to patient throughput. Siemens Healthineers, GE HealthCare, and Philips Healthcare anchor this segment.

Instruments & Systems: USD 3.12 Billion in 2025. Hospital imaging-fleet upgrade cycles for MRI, CT, and PET scanners entering a major refresh window as systems purchased during the 2014–2016 expansion reach end-of-life.

BY TECHNOLOGY

Neuroimaging Technologies: Dominant technology with USD 6.19 Billion in 2025. MRI, CT, and PET scanners represent the highest-value installed base, supported by fleet upgrades to AI-enabled MRI and PET-CT platforms.

Neuroinformatics & AI Analytics: Fastest-growing technology class at 12.3% CAGR (2026–2035). Real-time decision support integration, automated EEG spike sorting, and cloud-based PACS integration command premium pricing relative to legacy software.

BY CONDITION

Neurodegenerative Diseases: Dominant indication with ~37.3% revenue share in 2025. Alzheimer’s and Parkinson’s early-detection mandates drive structural demand for imaging and biomarker diagnostics.

Sleep Disorders: Fastest-growing condition segment at 11.2% CAGR (2026–2035). Home sleep-testing reimbursement growth and wearable actigraphy gain payer acceptance, shifting volumes away from hospital-based sleep labs.

Cerebrovascular Disorders: USD 2.14 Billion in 2025. Stroke-pathway time targets and thrombectomy protocols create urgent demand for rapid neuroimaging.

BY END USER

Hospitals & Surgical Centers: Largest segment at ~55.4% share in 2025. National hospital procurement through ministries of health and GPO tenders dominates volume, channeling inpatient neuroimaging and intraoperative neuromonitoring supply.

Diagnostic Laboratories & Imaging Centers: USD 2.48 Billion in 2025. Outpatient referral imaging volumes and centralized biomarker testing create steady demand.

Read Detailed Insights:

https://www.marketresearchfuture.com/reports/neurodiagnostics-market-8762

Regional Outlook

North America — Dominant Market (~38.5% Share, 2025)

The United States generates approximately 79.2% of North American Neurodiagnostics Market revenue, driven by CMS coverage decisions that expanded reimbursement for amyloid PET and blood-based Alzheimer’s biomarkers in 2024–2025. The NIH BRAIN Initiative’s USD 12 billion commitment through 2026 has compressed traditional adoption timelines and attracted private capital into cloud-enabled diagnostic platforms. Reimbursement breadth and Medicare coverage expansion support premium-priced AI-enabled imaging and biomarker demand that pooled-procurement regions cannot match.

Canada contributes through provincial imaging-fleet renewal programs at 12.5% of regional share, while Mexico is growing at 6.8% CAGR on INSABI-successor public health modernization, channeling capital toward diagnostic capacity in underserved states. North America’s leadership rests on reimbursement depth, mature clinical evidence requirements, and the structural shift toward AI-augmented and biomarker-integrated diagnostic workflows.

Europe — Second Largest (~27.0% Share, 2025)

Europe’s Neurodiagnostics Market reflects divergent national strategies under a harmonizing regulatory umbrella. Germany leads with 23.4% of regional revenue, driven by the hospital digitization law (KHZG) which allocated EUR 4.3 billion for digital-health infrastructure upgrades across 1,900 hospitals, and the Medizininformatik-Initiative digital-neurology platform. The UK is growing at 7.2% CAGR on the NHS Long Term Plan and AI diagnostic imaging fund, which has deployed over GBP 120 million since 2022 to integrate AI-assisted neuroimaging into stroke and epilepsy pathways.

Asia-Pacific — Fastest-Growing Region (10.0% CAGR, 2026–2035)

Asia-Pacific is the engine of the Neurodiagnostics Market. China holds the largest regional share at 34.8%, with the 14th Five-Year Plan for medical-equipment localization directing state-backed capital toward domestic MRI and EEG manufacturers, while simultaneously expanding diagnostic coverage under the National Healthcare Security Administration. India is growing at 11.2% CAGR on Ayushman Bharat hospital digitization, with rapidly growing private-hospital chains—Apollo, Fortis, and Narayana Health—deploying AI-enabled neuroimaging as a competitive differentiator.

Middle East & Africa — Emerging Opportunity (8.4% CAGR, 2026–2035)

The Middle East & Africa carries the widest diagnostic infrastructure gap and therefore significant opportunity. Saudi Arabia leads the region with 31.2% share, with Vision 2030 constructing 44 new hospitals and 100+ primary-care centers, each specified with advanced imaging suites, creating a concentrated procurement wave for the Neurodiagnostics Market. The UAE is growing at 9.6% CAGR on medical-tourism hub strategy, attracting patients from the broader Gulf and North Africa for complex neurological workups.

South America — Growing Presence (USD 0.58 Billion, 2025)

Brazil anchors South America’s Neurodiagnostics Market at ~58.6% of regional revenue, with SUS (Sistema Único de Saúde) public-health modernization channeling federal transfers toward MRI access in the Northeast and North macro-regions where diagnostic deserts persist, providing a stable demand floor that smooths regional forecasts. Argentina is growing at 7.4% CAGR on university-hospital fleet upgrades.

Competitive Landscape and Recent Developments

The Neurodiagnostics Market is moderately concentrated, with an estimated Herfindahl-Hirschman Index in the 800–1,200 range and the top five companies projected to account for 48–55% of global revenues. Concentration is highest in high-income segments where regulatory and manufacturing barriers are steep; the pooled-procurement tier is more fragmented as regional producers compete on price. Since 2023, M&A has accelerated as incumbents buy AI analytics firms to enhance their digital portfolios.

The competitive landscape is stratified between full-spectrum imaging OEMs serving hospital and reference laboratory markets, electrophysiology specialists capturing epilepsy and sleep monitoring growth, and AI-software disruptors consolidating the neuroinformatics segment.

KEY COMPANIES AND RECENT MILESTONES

Siemens Healthineers (December 2025): Introduced the MAGNETOM Free.XL, a 0.55T helium-free MRI system designed to enhance interventional radiology workflows, eliminating annual helium refill costs of USD 20,000–40,000 and reducing five-year ownership costs by an estimated 25–30%. Estimated revenue share: ~12–16%.

GE HealthCare (2024–2025): AIR Recon DL platform expanded via continuous updates to cover nearly all anatomical imaging, anchoring a broad portfolio spanning imaging, monitoring, and digital diagnostics. SIGNA MRI series and Edison AI platform command premium positioning. Estimated revenue share: ~10–14%.

Philips Healthcare (2024–2025): Ingenia MRI, Neuro Suite, and IntelliSpace anchor an integrated diagnostics-to-informatics workflow provider strategy. Estimated revenue share: ~8–12%.

Nihon Kohden (2024–2025): EEG-1200 series and Neurofax platform anchor a leading electrophysiology specialist position in Asia-Pacific. Estimated revenue share: ~5–8%.

Future Outlook: 2026–2035

By 2030, AI-autonomous diagnostic reporting will become the operating system of neurodiagnostics delivery. AI is expected to play a critical role in neuroimaging by performing high-volume triage and preliminary analysis, allowing radiologists to focus on complex-case review. While professional bodies like the RSNA emphasize a ‘human-in-the-loop’ model—where AI augments rather than replaces human expertise—the Neurodiagnostics Market is increasingly bifurcating between high-efficiency, AI-native platforms and specialist-intensive workflows. This shift is reshaping hospital staffing models to prioritize the integration of AI-assisted diagnostic tools, creating a new business model layered on top of the core neurodiagnostics franchise.

Remote and ambulatory neurophysiology monitoring will reframe cost structures by the early 2030s. Wearable EEG patches and home-based sleep-study kits reduce hospital bed-days and enable continuous data capture over 72–168 hours, far exceeding the diagnostic window of a standard 30-minute in-lab recording. The Neurodiagnostics Market stands to benefit as payers incentivize outpatient-first care pathways. As per-device costs fall with scale, the addressable channel widens from centralized reference laboratories to primary-care clinics, emergency departments, and patient homes, extending neurodiagnostics beyond traditional settings.

More Related Research Insights:

https://www.marketresearchfuture.com/reports/brain-imaging-neuroimaging-market-12265

https://www.marketresearchfuture.com/reports/brain-monitoring-market-2288

https://www.marketresearchfuture.com/reports/neurology-devices-market-9768

https://www.marketresearchfuture.com/reports/electroencephalography-systems-devices-market-43185

https://www.marketresearchfuture.com/reports/electromyography-devices-market-43247

https://www.marketresearchfuture.com/reports/neuromodulation-devices-market-1337

https://www.marketresearchfuture.com/reports/neurovascular-devices-market-5544

https://www.marketresearchfuture.com/reports/epilepsy-devices-market-10427

https://www.marketresearchfuture.com/reports/neurology-devices-market-9768

Larry Wilson

WantStats Research And Media Pvt. Ltd.

+1 855-661-4441

email us here

Visit us on social media:

LinkedIn

Facebook

YouTube

X

Legal Disclaimer:

EIN Presswire provides this news content “as is” without warranty of any kind. We do not accept any responsibility or liability

for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this

article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

![]()

Media gallery